By: Jordan Hall

To invest in a house might the most difficult economic feats to-do now. Ascending home prices and you will relatively previously-growing interest levels has combined in order to create a significant obstacle to possess homebuyers. As a result, most of these individuals are tempted to slow down the count it set-out on the very first purchase.

However, when you’re purchasing property may be more challenging than in age prior, placing at least 20% upon your home is nonetheless a good idea and you can arrives with many perhaps not-so-apparent masters. Let us discuss exactly what those individuals masters are.

The fresh Unanticipated Advantages of Placing 20% Down

The huge benefits start even before you close on the new home. Since the homebuying market is so aggressive, vendors examine the new even offers they receive in detail. They want to know that the possibility customer of the home comes with the most readily useful threat of addressing the fresh closing dining table effectively. One of the better indications of this ‘s the size of brand new deposit.

A deposit of at least 20% reveals their strength while the a purchaser, showing you have this new economic wherewithal so you can browse many prospective dangers between price and you can closing. These may tend to be assessment activities, unanticipated repairs, amaze borrowing issues, otherwise interest rate buydowns.

Because a real property representative of nearly ten years, I will to make sure your among the first issues representatives and sellers glance at inside the contrasting an offer ‘s https://availableloan.net/loans/signature-loans/ the sized the new recommended downpayment. Twenty % indicators your a highly-heeled client, economically willing to perform the required steps to close to the home, and can render your own bring a base facing fighting buyers. Which is a big deal.

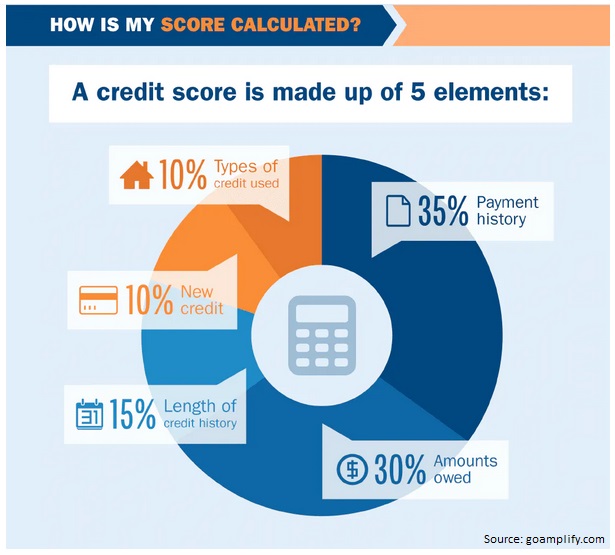

PMI represents “personal mortgage insurance coverage.” No-one loves investing insurance policies, however, it adaptation try tough than usual it protects the financial institution and will be offering no positive points to you given that the resident. And it is not cheap. NerdWallet reports it can easily run of up to .46 to one.5% of your original annual loan amount. Which is hundreds of dollars four weeks for most someone. So, why should some one shell out the dough? Well, as they need. PMI required into the the FHA and you will old-fashioned funds which have faster than a keen loan-to-worth ratio. But smart homeowners is eliminate it entirely from the placing no less than 20% down on the first get. This 1 move will save you tens and thousands of bucks over the life of your loan. Additionally, it conserves that money to help you spend the money for mortgage considerably faster.

The largest advantage of placing at least 20% upon a property is just one that people probably talk in regards to the least. This is simply the lower worry that good-sized security provides. Your residence is to include balances and defense into life not stress and you will proper care.

It is a straightforward equation, but the conclusion is the fact that the huge the newest down-payment for the your home, small your general financial and you may relevant monthly payment could be. Many loan providers will even render a reduced interest rate to the people which have a much bigger downpayment.

All of this results in a in check domestic payment and you can finest possibilities to pay off your mortgage more easily. This will reduce the attract you only pay complete and permit more of resources to get dedicated to building wide range or even.

If you are home prices possess risen consistently for some out-of Western history, there have been short-term pullback symptoms (see 2008). Which downturn, unfortunately, ravaged of numerous homeowners with slim guarantee. You do not want a dip from inside the really worth otherwise a beneficial hiccup during the the business to leave your underwater and you can less than economic pressure. A security support suppresses this case.

Additionally, it means that if you would like offer your house from inside the a pinch, you will have the fresh new crisis, of a lot property owners got stuck inside their property whenever values dipped. It’s hard to market anything, especially your home once you owe over it’s well worth. But getting 20% down aids in preventing it condition and ensures your house will stay a true blessing and never getting an albatross doing your neck.

Let’s perhaps not make bones regarding it. Putting 20% down try a high buy in this housing market. This may require you just like the good homebuyer to keep a bit stretched or slender you buy finances. not, performing this will allow you to go into the field off an effective effective standing, permitting your residence in order to subscribe to debt well-getting in the place of detracting from it. Owning a home try a lengthy-term online game, together with advantages commonly accrue for decades in the future.